ANC pulls further ahead of the DA…

23 March 2026 — Where does the latest polling place political parties? What impact will rising fuel prices have on logistics? How might they affect inflation and interest rates? How should President Ramaphosa’s latest remarks on growth and investment be interpreted? What does the lower gold price mean for markets and the fiscus?

Welcome to the weekly Risk Alert from the Centre for Risk Analysis — 23 March 2026

ANC pulls further ahead of the DA…

The latest nationwide opinion polling, conducted in February and early March by the Social Research Foundation and The Common Sense, finds that 39% of registered voters would vote for the African National Congress (ANC) if local government elections were held today, up two percentage points from the 37% support found in the previous November 2025 survey.

The Democratic Alliance (DA), by contrast, has dropped by four percentage points over the same period, from 32% to 28%. As a result, the ANC has pulled ahead of the DA, widening the gap between South Africa’s two largest parties from five points to eleven points.

Far behind are the uMkhonto weSizwe Party (MK) at 10%, the Economic Freedom Fighters (EFF) on 6%, and the Inkatha Freedom Party (IFP) on 5%. The Freedom Front Plus (FF+) is on 4%, while ActionSA and the Patriotic Alliance (PA) are both on 3%.

The national poll was conducted among a representative sample of 2,222 registered voters, producing a margin of error of 2.1%. Polling focusing specifically on Johannesburg, Tshwane and eThekwini was also conducted. Here the margin of error was 4.4% because the samples were smaller.

… but is in trouble in the metros

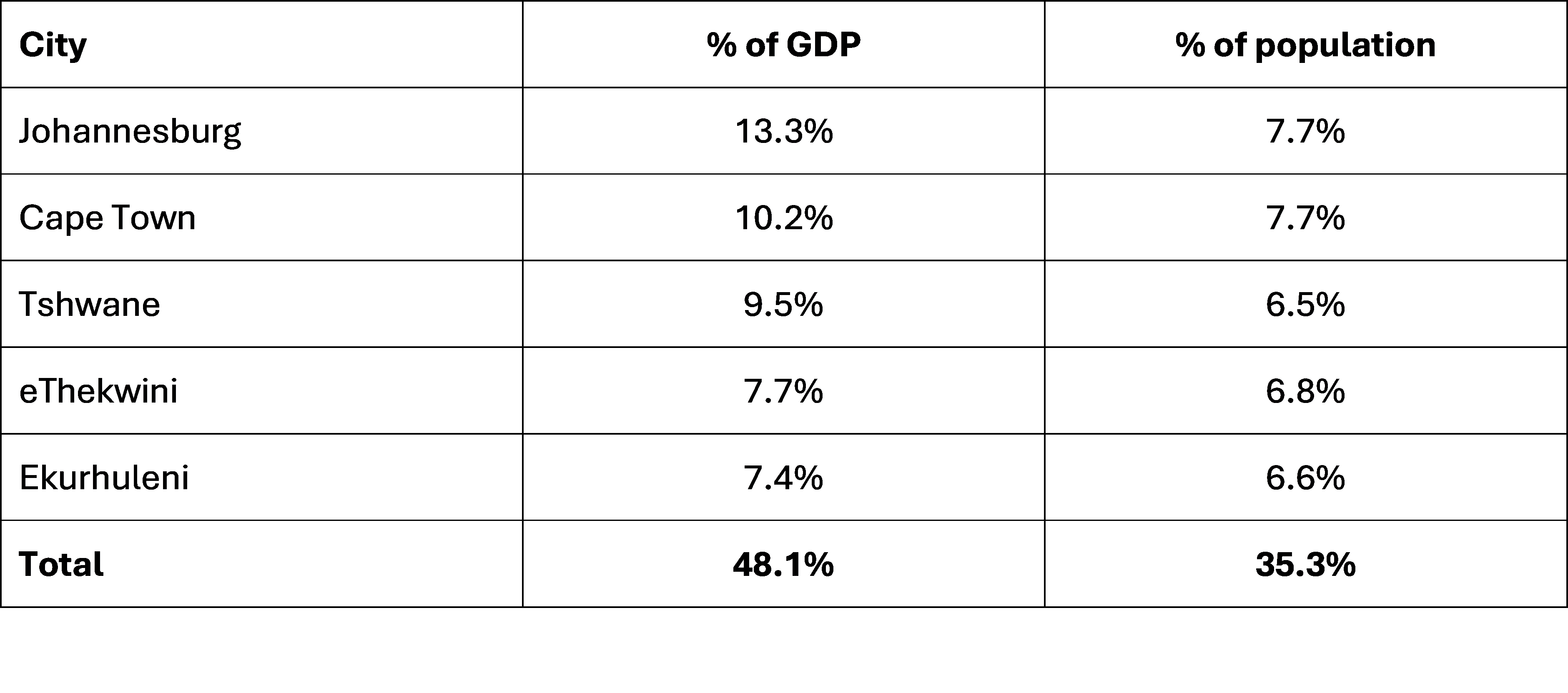

While superficially, the polling results look favourable for the ANC, a closer look suggests a different story. In Johannesburg, the DA is leading the ANC, 39% to 30%. They are followed by ActionSA at 10% and MK at 8%.

The DA’s relatively strong showing is being boosted by Helen Zille’s high-energy mayoral campaign, while support for the ANC is depressed by ongoing service delivery disasters, with large parts of the city once again without water for several days, refuse collection not having taken place for around three weeks across swathes of the city, and area-wide electricity outages, potholes, broken streetlights and non-functioning robots a perennial problem. This comes as the ANC-led council last week budgeted R10 billion to increase the salaries of the city’s municipal workers.

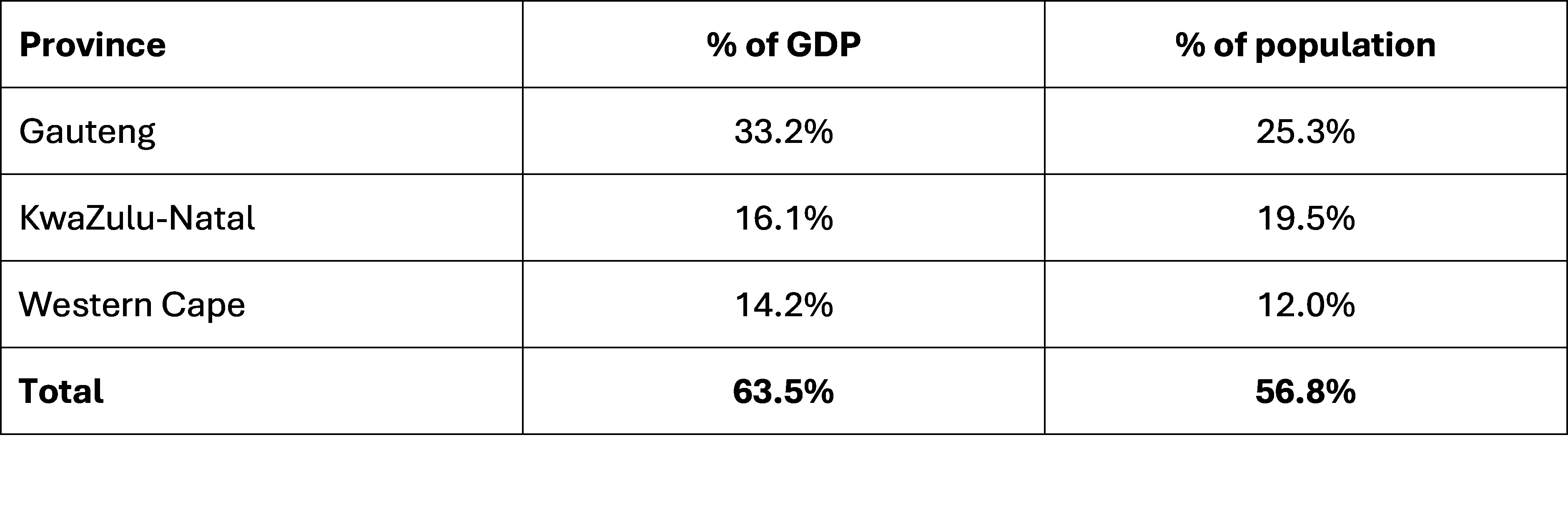

In eThekwini, if the polling is anything to go by, the ANC is at risk of getting wiped out. Just 8% of respondents said they would vote for it. The most popular party in the city was the MK, at 44%, followed by the DA at 28%, while 18% said they would vote for the IFP. All other parties were polled at below 4% and therefore below the margin of error. eThekwini accounts for 7.7% of national GDP and 6.8% of the country’s population.

The reason this matters is that the ANC is trending towards losing power in key population centres that are South Africa’s plumpest political fruit. If this plays out as current polling trends suggest, the party would then be relegated to the more rural, poorer, less economically productive parts of the country, with the loss of some metros in the local government elections presaging a subsequent loss of provinces such as Gauteng and KwaZulu-Natal in the 2029 national and provincial elections.

Key provinces

Key cities

Trucking in trouble

The current volatility in global oil markets is making itself felt locally. Last week, a widely circulated alert listed multiple petrol stations and depots that had run out of 50ppm diesel, with affected areas spanning Gauteng, the Free State, North West, Northern Cape, and Western Cape.

This came as the Central Energy Fund published the latest data on fuel pricing, which suggests that the price of petrol could increase by up to R5.41 per litre from 1 April, while that of diesel could rise by R8.84 per litre. Both increases will include the higher fuel levies announced by the finance minister during the budget speech.

“Higher fuel prices increase the cost of every kilometre travelled by a transporter,” says Thato Moloi, president of SAPICS, the South African supply chain industry body. “That cost moves through the entire supply chain and eventually shows up on store shelves.”

The Department of Mineral and Petroleum Resources has indicated that fuel supplies for March and early April 2026 were secured before the conflict in Iran. It has not, however, confirmed supply arrangements beyond that window — leaving uncertainty heading into the Easter period.

South Africa’s supply chains are diesel-dependent, and that dependency is currently exposed with uncertainties in the near future. Diesel underpins the movement of virtually everything: trucks, freight rail, port equipment, and agricultural machinery all run on it. And when diesel prices rise, logistics costs follow.

Inflation slows to 3% in February, but spike likely in April

Official data released on Wednesday showed annual inflation slowing to 3% in February, down from the 3.5% recorded in January. However, prices are expected to start rising more rapidly from April, as the higher oil price makes itself felt through more expensive fuel and logistics costs. Households expect prices to rise by 5.4% over the next twelve months. Against this backdrop, it is unlikely that the South African Reserve Bank will cut interest rates at its next meeting, later this week.

Consumer food price inflation slowed to 3.7% in February 2026, down from 4.0% in January, but fuel prices remain a major upside risk because they account for a large share of distribution costs. Fuel and fertiliser costs have a delayed effect on food price inflation. Even though fuel accounts for 13% of the input costs of grain farmers, the farmers cannot pass on this cost to consumers except by adjusting their planting decisions in the next season.

Ramaphosa pays lip service to growth

At a News24 event on 19 March, President Cyril Ramaphosa said: “We know that growth creates jobs. When our economy has grown in the past, unemployment has reduced. That is why we are focused on implementing economic reforms and creating an environment for businesses to invest.”

While it is to be welcomed that Mr Ramaphosa is talking the language of economic growth and investment, the remainder of his speech showed little that was new.

The president’s plans to grow the economy are predicated largely on spending money — for example, R1 trillion in infrastructure spending over the next three years — and on more government interventions, for example job schemes such as the Presidential Employment Stimulus and the Youth Employment Service, plus extremely delayed responses to pressing emergencies, such as the formation of a National Water Crisis Committee.

Also last week, Mr Ramaphosa’s deputy, Paul Mashatile, reiterated the government’s firm commitment to race-based laws such as Broad-Based Black Economic Empowerment (B-BBEE) while drawing attention to a two-phase review of the scheme, currently underway.

While wishing for more job creation, economic growth and greater equality — things that B-BBEE has failed to deliver — Mr Mashatile announced that the government would be strengthening B-BBEE and said that abandoning B‑BBEE was “not an option”.

For context, SRF polling asked respondents if they would support replacing race-based BEE with a poverty-based policy. A majority of supporters of each of the four largest political parties agreed that they would: 52% of MK voters, 58% of EFF voters, 61% of ANC voters, and 87% of DA voters.

Gold loses its shine

The gold price fell 15% in three weeks, from $5,300 an ounce on 2 March to $4,488 on 20 March. Together with rising oil prices, this suggests markets now expect the US-Israel-Iran war to end more quickly than feared. The drop has hit the JSE All-Share hard, pushing it from above 128,000 at the end of February to 110,070 on 20 March.

More importantly, a persistently lower gold price would remove the extra mining revenue — roughly R30-40 billion projected for 2026/27 — that helped cover budget gaps and hid deeper problems. The next twelve months will show whether South Africa can grow above 1% without this commodity windfall, or whether the recent gains were mostly a temporary lift from higher resource prices and consumer spending.